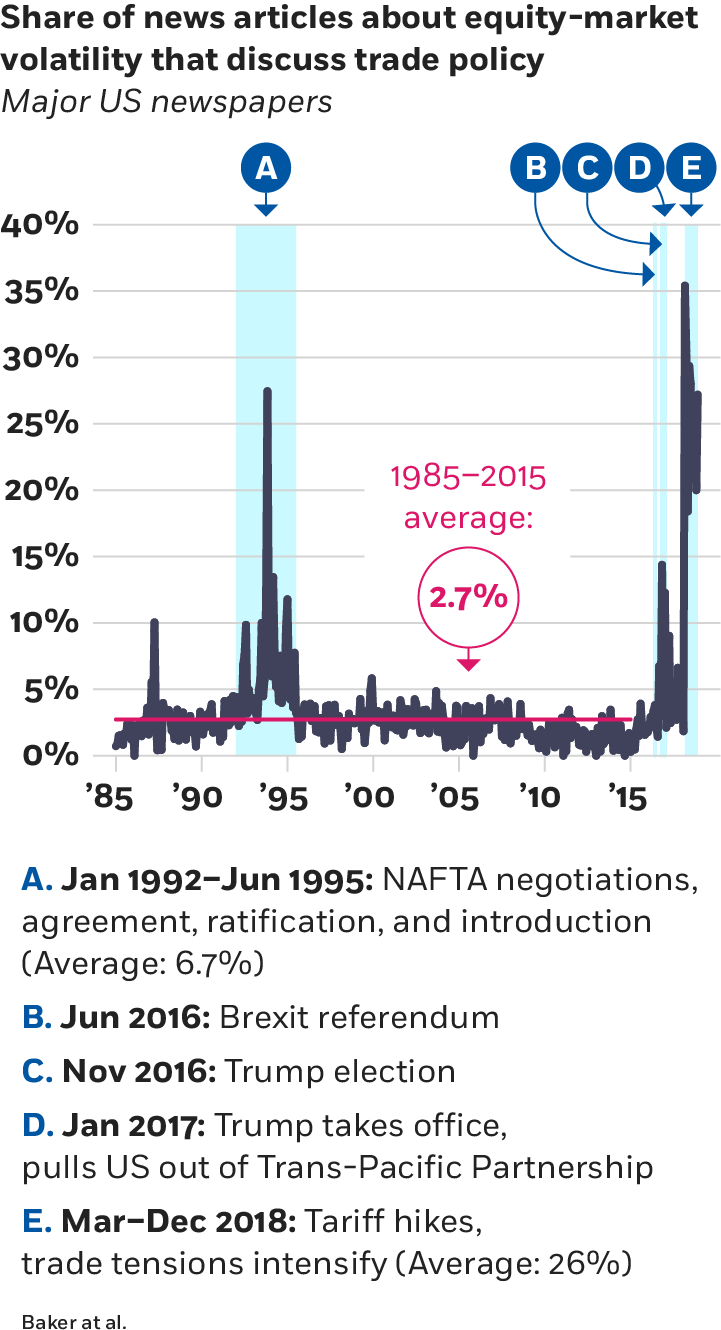

How tariff hikes and trade-policy tensions affected US companies’ 2018 capital investment spending

Calculations using Survey of Business Uncertainty data, January 2019

| |

Private sector |

Manufacturing |

| Percentage change |

-1.2% |

-4.2% |

| Change in dollars |

-$32.5 billion |

-$22 billion |

| Survey responses |

337 |

95 |

Altig et al.; Survey of Business Uncertainty by Federal Reserve Bank of Atlanta, Stanford, Chicago Booth

We estimate that tariff hikes and trade-policy tensions lowered gross investment in 2018 by 1 percent in the private sector and 4 percent in the manufacturing sector. The larger response for manufacturing makes sense, given the sector’s relatively high exposure to international trade. In constructing these estimates, we considered companies that raised and lowered investment due to trade policy, and we weighted each company by its size.

To estimate the dollar impact of trade-policy developments, we multiplied the percentage effects by aggregate investment values. The resulting amounts for business investment in 2018—minus $32.5 billion for the private sector and $22 billion for manufacturing—are quite small compared to the $21 trillion size of the US economy.

We also asked forward-looking questions about the potential impact of trade-policy worries on future business investment. Companies anticipate somewhat larger, but still modest, effects of trade-policy developments on their capital expenditures this year. (The Atlanta Fed’s David Altig, Brent Meyer, and Nick Parker; Stanford’s Bloom; and I more fully discuss our conclusions on the basis of these forward-looking survey questions in a blog post for the Atlanta Fed, “Tariff Worries and US Business Investment, Take Two.”)

How can we square the small effects of trade-policy developments on US business investment with their recently large role in US stock market volatility? The answer has at least two parts. First, many companies listed on the US stock market, especially larger ones, have significant commercial interests abroad. These interests include foreign production facilities that export to the US, supply chains that run through China, and brand values and distribution networks in foreign economies. Tariffs and trade-war concerns put these commercial interests at risk and reduce their value. That, in turn, lowers the equity value of the company on the US stock market, even when it has little impact on the company’s US domestic operations.

Second, our survey evidence may not capture the indirect effects of trade policy on domestic investment. For example, when US tariff hikes weaken foreign economies, they also lower demand for US exports. Companies in the survey may attribute these demand declines to overall economic conditions rather than trade-policy developments.

What should we expect looking ahead? Trade-policy news and anxieties will remain an important source of stock market volatility so long as the US is embroiled in trade-policy conflicts with its major trading partners. Higher tariffs and an uncertain trade-policy outlook will also dampen domestic investment by US companies. But the effects on domestic business investment will stay small, barring a dramatic escalation of tariffs and other trade barriers.

Steven J. Davis is William H. Abbott Distinguished Service Professor of International Business and Economics at Chicago Booth and senior fellow at the Hoover Institution.