How Computational Linguistics Can Reveal Company Strategy

The language of earnings calls can help diagnose economic outcomes associated with periods of uncertainty.

How Computational Linguistics Can Reveal Company Strategy

Matt Chase

Sometimes it’s easy on an earnings call to spot the metrics that portend good or bad things for a company. Revenues were unexpectedly high. Operating costs have doubled. But what does it mean when a CEO’s adverb density is low? Or if her words per sentence are high? What’s the significance of a CEO consistently referring questions to her team? Is heavy use of euphemisms a bad sign?

A growing body of academic research suggests that while talk may be cheap, language—in particular, the language used during earnings calls—can be quite valuable. Seemingly boring transcripts from what are often hour-long calls can include spontaneous word choices that offer insights on everything from executive character traits to the inner workings of a firm. Researchers are parsing the language from tens of thousands of earnings-call transcripts and cross-referencing these data with firm financials, biographical data about executives, linguistics research, and even the psychology of speech. When CEOs talk, researchers listen—and investors can profit from their findings.

Earnings calls are the periodic conference calls a company’s executives hold with investors and analysts to discuss financial results and answer questions. The calls give managers a chance to provide context, or even spin, for their financials, and they also help companies stay on the right side of transparency regulations. Remarks for the first half of a given call are likely to be well rehearsed, or even prerecorded. But dialogue during the second half of the call, the question-and-answer portion, tends to be more reflexive, despite days of preparation from the management team.

“There’s some degree of off-the-cuff exchange between market participants and executives—it provides a window into the firm,” says Chicago Booth’s Michael Minnis, who mined earnings-call transcripts with the University of Michigan’s Feng Li (now at the Shanghai Advanced Institute of Finance) and Venky Nagar, as well as incoming dean at Chicago Booth Madhav Rajan, to see what they suggested about the inner workings of the corresponding businesses.

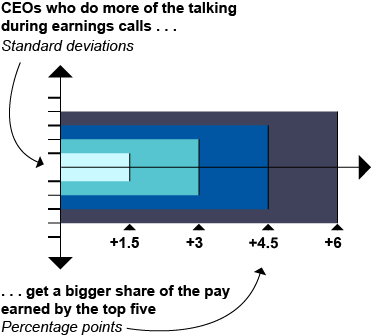

In the study, the researchers used how much and how often the chief executive spoke in contrast to other firm employees as an indicator of how knowledge is dispersed throughout the firm. In analyzing 17,419 transcripts, Li, Minnis, Nagar, and Rajan could evaluate how knowledge was distributed among various executive teams and hypothesize how that distribution affected financials.

Their research indicates that the chief executives who spoke more—presumably because they were more knowledgeable—also tended to earn more relative to the rest of the executive team. What’s more, firms that had mismatched compensation strategies (i.e., chief executives who talked more but got paid less) had lower firm value than those where talk time and compensation were aligned.

The researchers were also able to draw more-detailed observations about executives using the call transcripts. For example, CEOs without a Chartered Financial Analyst designation often deferred to the CFO, demonstrating a lack of comfort with financial topics. And as was the case with CEOs, CFOs who spoke more compared to their peers received higher compensation.

Where CEOs stand among other executives

Li et al., 2014

But reading between the lines of earnings calls doesn’t just mean adding up airtime. The language the management team uses can signal how it feels about its results—or how it expects the market to react to them.

For instance, when a chief executive tells analysts that “lumpiness,” “headwinds,” or a “wait-and-see” period is on the way, it may be time for an adjustment in your portfolio. Euphemisms such as these can obscure the details of bad news, and research suggests that greater use of them is associated with lower stock prices in the quarter ahead, even after taking into account the already disclosed financial results.

“The purpose of using euphemisms is to mislead,” says Kate Suslava, a Rutgers University PhD accounting candidate with a background in linguistics, who studied the link between euphemisms and stock performance by analyzing earnings-call transcripts. “They don’t want to scare off investors.”

The language of earnings calls can help diagnose economic outcomes associated with periods of uncertainty.

How Computational Linguistics Can Reveal Company StrategyAnd in fact, euphemisms are effective for precisely that purpose: Suslava finds that euphemistic earnings calls tend to significantly delay negative investor reaction.

On the flip side, analysts use euphemisms to soften their questions in the hope of getting those questions answered, she adds. Analysts “don’t want to ask tough questions directly, because it might cause an unpleasant reaction” from management.

As Suslava’s research demonstrates, the linguistic features of a call can provide valuable glimpses into a particular firm. But they can also shed light on its leaders. Harvard’s Ian D. Gow, Chicago Booth’s Steve Kaplan and Anastasia A. Zakolyukina, and David F. Larcker of Stanford used the language that appears in earnings-call transcripts to decipher the personality of chief executives, and then matched that to firm performance and investment and financing choices.

Prior research suggests that “personality traits are predictive of patterns of behavior,” says Zakolyukina, citing research from University of Illinois’s Brent W. Roberts. She explains that those traits can be difficult to measure in high-profile executives: “We suggest using earnings-call transcripts to estimate CEOs’ personality trait scores.”

CEOs’ most common lingusitic features in conference calls, categorized by “Big Five” personality traits

Scale: Prevalence of each feature relative to No. 1 on the list

Gow et al., 2016

The team categorized the personalities of 4,700 CEOs using the traits that make up the “Big Five,” a widely accepted framework for classifying personality characteristics: conscientiousness, extroversion, agreeableness, neuroticism, and openness to experience. To do so, they searched for 33 linguistic features that they associated with these various personality types. For example, CEOs who were agreeable tended to use adverbs, fewer words per sentence, and vague quantifiers during the question-and-answer sessions. Extroverted CEOs, on the other hand, used fewer quantifiers, fewer words per sentence, and more so-called anxiety words, such as “worried” or “fearful.”

The researchers used their findings about executive personality traits to assess how those traits are associated with firm performance. Their findings suggest numerous connections between the characteristics of CEOs and the behaviors of the companies they lead. For example, the companies of CEOs who have extroverted personalities, as observed in the words used in the transcripts, were more likely to have lower cash flows and lower returns on assets. Top executives deemed to be more conscientious tended to run slower-growth companies, while those whose dominant personality trait was openness had companies with a greater focus on R&D.

In addition to providing insight into executives and firms, the language of conference calls can provide cues to help listeners pick up on important information. Research by Rutgers’s Dan Palmon and Rutgers PhD candidate Ke Xu, along with Bentley University’s Ari Yezegel, looked at disclosures before and after the word “but” during question-and-answer sessions, and their respective impact on stock prices. The study finds that what comes after “but”—the so-called contrastive word—has more influence on market reaction than what comes before.

The use of contrastive words is a way to provide unexpected bits of information during the latter portion of the call to address analyst concerns. Ultimately, the information is used in a corrective manner to clarify unfavorable revelations, according to the findings. “The use of contrastive words can provide favorable counter expectation information to reverse investors’ perception of seemingly unfavorable financial performance,” the researchers write.

Mining data from the transcripts of earnings calls wasn’t always so simple. Twenty years ago, transcripts weren’t as widely available as they are today. But in 2000, the US Securities and Exchange Commission established Reg FD, or Regulation Fair Disclosure, which forbids publicly traded companies from sharing “material nonpublic” information with analysts and investors without making it public at the same time. Best practices dictate that compliant firms make earnings calls available to the public via transcript or audio.

As a result, there has been a growing interest in these easily accessible quarterly disclosures—and not just from those who have equity in the companies being discussed. Research from Columbia University’s Anne Heinrichs, Harvard doctoral candidate Jihwon Park, and Harvard’s Eugene Soltes indicates that in addition to sell-side analysts and the companies’ current investors, institutional investors without any position in the firm are often listening—in fact, on average, half of buy-side consumers listening to or reading the transcript of an earnings call do not hold the firm’s securities at the time they’re doing so. “We find that much of institutional buy-side consumption [of earnings calls] actually arises from non-holders who may consider [making] an investment or who use the call to fulfill other informational needs,” Heinrichs, Park, and Soltes write.

There is also a broader interest in firm-initiated news, according to the researchers, who find that consultants, firm suppliers and partners, bankers, and media all take an interest in these calls. And that interest is durable: of the earnings-call audio or transcript requests that the researchers studied, 82,000—about 7 percent of the total—were for calls that were three years old or older. “Market participants not only value public firm disclosures for their timeliness,” the researchers write, “but also as historical record for understanding the firm.”

Many executives are highly aware of the importance of what they say during earnings calls, and they can spend weeks getting ready for them—from rehearsing answers to strategizing about the order in which analysts are called upon for the question-and-answer portion. Others can be reluctant to set aside significant time to prepare for earnings calls, “and a few come into coaching sessions kicking and screaming,” says Jeff Leshay, a Chicago-based executive communications coach. Once they understand the value of prep work, however, “they learn to turn even the most challenging earnings-call questions into opportunities to build their brand.”

Leshay helps companies communicate using engaging anecdotes around the information disclosed during their earnings calls. He counsels clients on how to speak conversationally and with a genuine level of enthusiasm that helps the remarks feel unscripted—for instance, by speaking while standing and smiling, which can create an authoritative and enthusiastic tone that translates well over the phone. “They have to appeal to analysts on an emotional level,” he says, while also providing the data and details those analysts need to build their models.

Other strategies are more logistical than emotional. The National Investor Relations Institute (NIRI), a professional association for investment-relations professionals, helps run data on best practices for holding calls. For example, calls are most often held on Thursdays, with earnings released just before the market opens for the day.

Companies have responded to the increased interest in earnings calls. In 2016, 97 percent of public companies conducted calls, compared to 80 percent in 1996, according to a 2016 NIRI research report. There’s also been an uptick in CEO attendance: Minnis and his coauthors find that 93 percent of chief executives attended calls in 2007, up from 86 percent in 2003, and that the portion of the talking done by the CEO went up as well.

But the competition for special access to public companies is changing, says Minnis. While earnings calls must be available to the public, investors are flocking to conferences hosted by big financial institutions, which give investors a closed venue for communication. “At conferences, executives can provide pieces of the mosaic about the company that an expert investor might find informative,” Minnis says, though he adds that technically, Reg FD doesn’t allow any extra information to be released.

Most frequently used euphemisms

Executives’ use of euphemisms in earnings calls can obscure the details of bad news and delay negative investor reaction.

| Percentage of calls in which term is used | Average number of times repeated |

|---|---|

Suslava, 2017

Ultimately, investors and analysts are looking for access to company executives—opportunities to interact one-on-one, outside the context of an earnings call, in settings where remarks are likely to be unrehearsed. The result is earnings calls that are increasingly augmented with other venues for interaction. “The market for selective access has opened up in other ways,” Minnis says.

The popularity of alternative venues for communicating with investors suggests firms continue to get savvier about how they release information. They may also be getting more cautious. In 2016, 15 percent of companies said that they prerecord formal earnings-call comments prior to hosting a live question-and-answer session, compared to 10 percent in 2014, according to NIRI research. What’s more, only 11 percent of companies that prerecord remarks disclosed that they do so. And 64 percent of companies said they now host invite-only postearnings calls for analysts and/or top shareholders, a number that has increased steadily, according to the data.

But even as the words become more rehearsed, there are other ways to keep digging, say researchers. Some are hoping that audio recordings of the earnings calls, as opposed to transcripts, will soon be easily analyzed in bulk. Focusing research on intonation, awkward pauses, and other auditory details can provide even more information about an executive’s temperament. “Even the pause between the question and answer could be predictive,” says Zakolyukina.

In addition to audio files, there is the possibility that in the future, firms will make video files available, which would permit analysis of things such as mannerisms or nervous tics.

“We’ve just started to scratch the surface,” Zakolyukina says.

Researchers are using machine-learning models to improve how investors allocate their funds.

Three Ways A.I. Can Improve Decision-Making

Their insights changed the modern understanding of banks.

What the Latest Nobel Winners Taught Us

Doing business with suppliers in another country can expose a US company to increased risks, but it can also provide a buffer against local shocks.

Global Supply Chains Can Hurt a Company’s CreditYour Privacy

We want to demonstrate our commitment to your privacy. Please review Chicago Booth's privacy notice, which provides information explaining how and why we collect particular information when you visit our website.