What’s the Fundamental Value of a Bitcoin?

Despite the rapid upswing in bitcoin’s price, predicting the currency’s future may still prove a daunting task.

What’s the Fundamental Value of a Bitcoin?

Dan Page

Everything associated with Bitcoin became a little more interesting when the cryptocurrency’s value skyrocketed, doubling in less than a month to more than $17,500 by mid-December 2017. But even though many investors remain skeptical about Bitcoin, blockchain—the open-source code behind it—has drawn interest from a diverse set of household names, including Citigroup, UPS, and Walmart.

Walmart may view blockchain—which was popularized in 2009 by Bitcoin’s anonymous founder—as a way to follow a crate of frozen tilapia from Shanghai to South Dakota. For Maersk, the Danish shipping conglomerate, blockchain could help it confirm that a vital customs form for a cargo ship in Dubai, United Arab Emirates, has been signed. A blogger in Mexico City could rely on the technology to accept low-fee micropayments from appreciative readers in Milan.

Despite the rapid upswing in bitcoin’s price, predicting the currency’s future may still prove a daunting task.

What’s the Fundamental Value of a Bitcoin?

Like many things digital, Bitcoin has the potential either to transform the world or to be largely ignored by it.

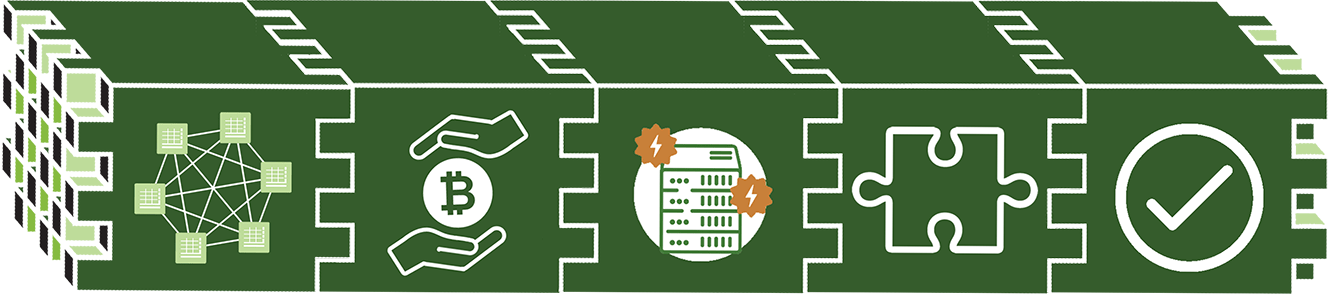

Is Bitcoin the World’s Next Major Currency?But there’s a drawback: blockchains have the potential to increase collusion, according to Chicago Booth’s Lin William Cong and Zhiguo He. The researchers’ modeling, part of their research into how blockchains might affect competition, suggests that the way blockchains work as a decentralized ledger involves distributing more information, which could make it easier for competitors to quietly and often tacitly collude to keep prices high, ultimately to the detriment of consumers. But Cong and He propose a few potential remedies.

Blockchain is less well-known than Bitcoin but may have more staying power. Its main functionality is providing “decentralized consensus,” say Cong and He. In most societies and economies, parties in a contract rely on a government, court, or other third-party arbitrator to essentially oversee and enforce rules in private contracts—to provide consensus, as the researchers put it. Blockchain provides that function in a more decentralized manner by generating, storing, and distributing the record of rules and regulations.

Its strength as a bookkeeping method stems from the way records are verified, linked, and stored across a network of computers. In a simplified example, the record of a Wednesday morning sale of 10 bitcoins might be lumped with other transactions made the same day. This block will be verified when a self-selected participant in the chain of transactions—known as a Bitcoin miner—solves a difficult cryptographic puzzle that an algorithm in the source code creates specifically for this block of transactions.

The puzzle for the Wednesday block is partly built on the solution to the puzzle used to verify the immediately previous block, say the one containing all Tuesday transactions. And the Wednesday solution would in turn be employed in a new puzzle to verify a Thursday block. This makes the ledger difficult if not impossible to hack. Altering the Wednesday record cannot be achieved without altering records up and down the chain.

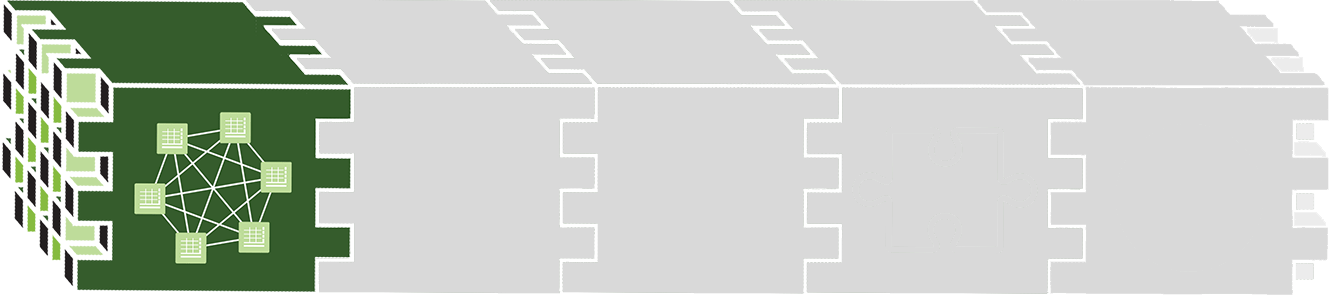

The basics of blockchain

Click the arrows below to see how blockchain technology creates an accurate historical ledger of transactions.

A decentralized network of record keepers, rather than a central intermediary such as a government agency or bank, maintains the ledger.

When two parties want to use the blockchain to record a transaction, they broadcast a request to everyone in the network. It is combined with other recent transaction requests into a "block."

Many members of the network—in Bitcoin circles, they're known as miners—use powerful computer setups to compete for the right to add the block to the blockchain.

The miners race to solve a complex cryptographic puzzle, which is part of the code required to add the new block to the blockchain. They also check whether the transactions are valid, reconciling them with past records on the blockchain to verify that the funds exist.

The block is added, making the transactions official, and the winning miner receives an award—for example, transaction fees. Everyone in the network updates their copies of the blockchain.

1 of 1

The miners are individuals willing to pour computing power into solving these puzzles in exchange for newly issued bitcoins and users’ transaction fees. The fees are relatively low compared with those of banks or other financial institutions. There is no official count of Bitcoin miners, and estimates by currency watchers range widely, from 5,000 to 150,000 around the world. The fact that every miner holds an up-to-date record of the chain adds to the technology’s robustness.

This makes for the combination of high security and low fees (for now) that a currency-trading platform needs. For other business applications, the blockchain offers advances on the old ways of doing things.

Take the Walmart example. For reasons ranging from reputation to protection against liability, the retailer wants to ensure that the tilapia it sells meets certain quality standards. Among other considerations, once-frozen fish should stay frozen until a customer defrosts it himself. Currently, ensuring this requires Walmart to keep tabs on a line of middlemen making strings of promises confirmed by anything from legally binding contracts to handshakes, which is arduous and expensive.

Using the blockchain, however, Walmart could sign contracts directly and in real time with everyone from a fisherman to a wholesale-seafood-market manager, a packager, a US customs agent, and a long-haul trucker. Fees would be minimal, and the paperwork eliminated entirely. The digital contracts would also be tamperproof. As Cong and He highlight, such smart contracting solves the trust issue and encourages other parties to enter and compete in the market. Thanks to the robust system of oversight and enforcement, Walmart can trust that contracts will be executed, even by new companies it hasn’t done business with before. If a company it does business with fails to meet the terms of its contract, the company is penalized, or the contracted fee isn’t transferred.

However, the researchers identify a potential trade-off to these advantages: the possibility of cartel risk. Blockchains won’t necessarily lead to cartels, but Cong and He point out that cartels could arise in certain conditions.

Blockchain idealists would have all transactions stored on one chain—the one that already exists, thanks to Bitcoin. This would create a massive, democratic, stable, and unified public record. But most companies don’t buy into this vision. Critics say this is because they want to control the chains, keeping out new competitors by using private or “permissioned” blockchains.

Last year, IBM built a blockchain for clearing credit-default swaps, a form of financial derivative. Bloomberg View columnist Matt Levine wrote about a permissioned blockchain being designed for the Depository Trust & Clearing Corporation, an organization that provides clearing and settlement services to the financial industry.

“You and I can’t just walk in and trade derivatives over the new DTCC blockchain,” Levine wrote. “It’s for the big incumbent players who are part of the DTCC consortium anyway. There is no disruption, no disintermediation. The blockchain here is about perpetuating the existing intermediaries, not about replacing them.” In such private blockchains, new entrants would be kept out.

“Blockchains ... have profound economic implications on consensus generation, industrial organization, smart contract design, and anti-trust policy.”

Collusion could arise even in public blockchains, according to Cong and He. In the traditional way of doing things, without blockchains, information is limited, the researchers note. For example, a mortgage broker who loses customers doesn’t have an easy way of knowing whether they are being poached by rivals or whether fewer people are taking out mortgages across the market. As a result, she might try dropping her prices to guard against the possibility that a competitor is luring away customers with better rates. This kind of response increases competition and consumer welfare, the researchers say. Thus in a world without blockchains, the seller, to gain business, will abandon any tacit agreement to collude that might have previously existed between her and her competitors.

But on a public blockchain, more information becomes available regarding each participant on the chain. Because transactions are verified to reach decentralized consensus, sellers could infer the total number of transactions taking place in the market. So our mortgage seller could know whether she is losing out to a competitor or simply seeing the total customer base shrinking. If it’s an industry-wide decline in demand, she may be less inclined to cut prices. Thus, knowledge made possible by the blockchain could encourage tacit collusion—even though the transaction data is anonymous. Just as “no news is news,” write Cong and He, “even encrypted data are still data.”

One solution to this problem of sellers colluding on a blockchain would be to encourage multiple public blockchains to blossom. The researchers suggest that the least collusive blockchain would win the most transactions, with price-conscious customers veering away from collusive markets, thereby encouraging other blockchains to become less collusive to win customers. If a single blockchain emerged, regulators would have to step in because market forces wouldn’t block collusion, Cong and He say.

Regulators might demand access to the source code, or parts of the source code, gaining a scaffolding on which to build data-monitoring systems that analyze transaction and price trends to detect tacit collusion. Effective regulation might involve limiting a seller’s access to information. Our mortgage seller could take part in transactions on the blockchain but would not get to see all the transactions taking place, thus limiting her ability to estimate the size of the total market. In essence, it can be beneficial to separate blockchain users from the miners who are generating decentralized consensus, the researchers argue.

“If sellers can only use the blockchain for signing smart contracts with buyers, then they no longer have access to the aggregate activity information in the relevant market that facilitates collusion,” Cong and He write. Clearly, enough interest in blockchains exists that some of these solutions can be tested. And inevitably new solutions will arise. In the meantime, expect more companies to jump on the bandwagon at least to be part of the hottest new technology on the block.

“Blockchains are not merely database technology that reduces the cost of storing or sharing data,” the researchers write, “but have profound economic implications on consensus generation, industrial organization, smart contract design, and anti-trust policy.”

Lin William Cong and Zhiguo He, “Blockchain Disruption and Smart Contracts,” Working paper, October 2017.

A Q&A with Chicago Booth’s Dacheng Xiu on the implications of machine learning for the financial markets.

In Finance, Humans Were the First Machines

The growth of privately held businesses has some regulators and policy makers pondering whether to push for more financial transparency.

Is the US Economy ‘Going Dark’?

Why did prices for US Treasurys drop along with stock prices in the spring of 2020?

How Financial Regulation Fed a Treasury Bond CrisisYour Privacy

We want to demonstrate our commitment to your privacy. Please review Chicago Booth's privacy notice, which provides information explaining how and why we collect particular information when you visit our website.