Hostel, a guts-and-gore-filled horror movie released in 2005, might seem to offer little insight into the financial markets. But Professor Luigi Zingales employs an innovative methodology—including showing scenes from Hostel—to quantify the extent to which fear caused investors’ risk aversion to spike after the 2008–09 financial crisis, impeding their ability to make smart investment choices.

To test the extent of this postcrisis risk aversion, Zingales, along with Luigi Guiso of the Einaudi Institute for Economics and Finance and Paola Sapienza of Northwestern University, used a survey of bank clients, and then tested a hypothesis about its psychological roots in an experiment that uses a particularly gruesome excerpt from Hostel.

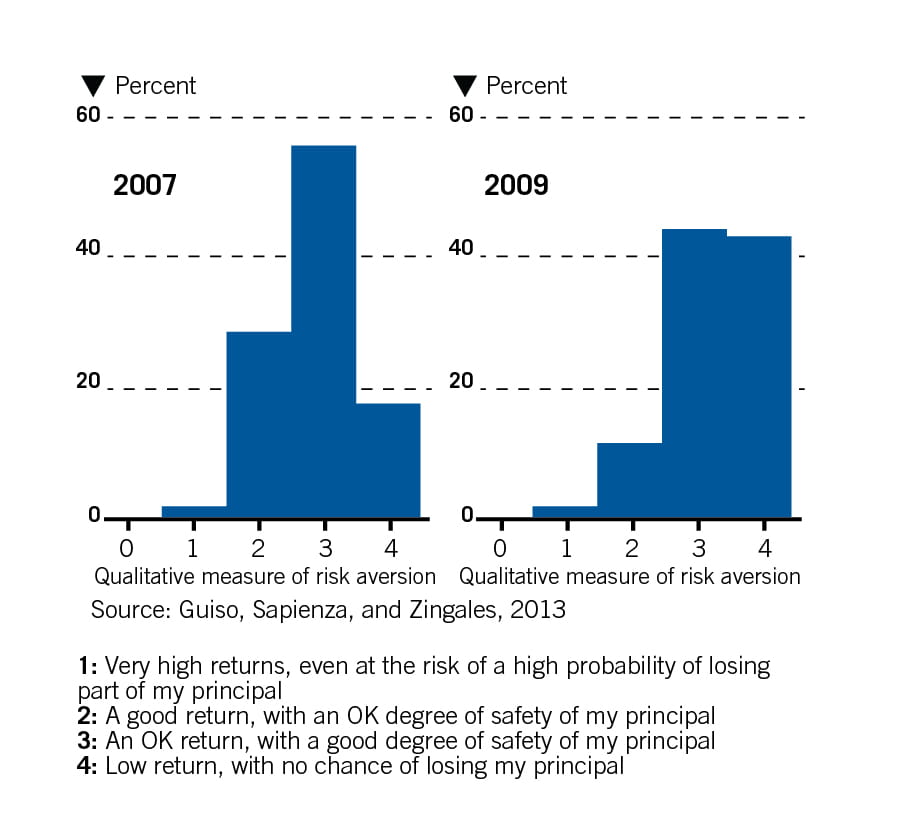

In the initial survey, the researchers gave two identical questionnaires to clients of an Italian bank. Participants received the first in January 2007, well before the crisis, and the second in June 2009, when the financial crisis was still raging. About one-third of the clients agreed to be reinterviewed in 2009, resulting in a dataset of 666 investors across both questionnaires. To be included in the survey, customers had to have at least €10,000 deposited at the bank at the end of 2006.

In both questionnaires, the first question, which the researchers call “the quantitative question,” reveals respondents’ confidence in winning €10,000 in a gamble, in which they have an equal probability of winning nothing. The second question, “the qualitative question,” illuminates investment objectives, such as whether respondents were looking for “very high returns, even at the risk of a high probability of losing part of the principal,” “an OK return with a good degree of safety on the principal,” or “low returns, but no chance of losing principal.”