A Winning Football Team Can Improve a University’s Science Research

Investments in research—including those financed by successful athletic programs—can pay financial dividends.

A Winning Football Team Can Improve a University’s Science Research

Clint Blowers

At private US colleges, the weighted average cost for tuition and fees is $32,405, according to the College Board, while members of the class of 2015 graduated with more than $35,000 in student loans, on average, the Wall Street Journal reported.

Student debt has become a policy issue in the US presidential campaign, but it’s not clear how the system should work. Should public-college tuition be completely free, or available to students without their taking on any debt? Should states, rather than the federal government, handle college finance, or should we steer more students away from college and toward less-expensive vocational programs?

Investments in research—including those financed by successful athletic programs—can pay financial dividends.

A Winning Football Team Can Improve a University’s Science Research

A big trade on transfers could reduce waste and disincentives.

Universal Basic Income Isn’t a Magic Bullet but It’s a StartTo understand how the United States could or should redesign college finance, look south, to Chile. To be sure, Chile does not greatly resemble the US. The South American country has a population of just 18 million, rather than the US’s 323 million. A dictatorship ruled the country between 1973 and 1990, and its economy is heavily tied to commodities, particularly copper. But when it comes to higher education and affordability, Chile and the US face many of the same challenges in trying to make college accessible and affordable to the middle class.

Chile, however, has made big higher education reforms. In 2006, its government greatly expanded the national student-loan program, in a bid to make college more affordable. When many students graduated with big debts and no jobs (and, in many cases, no degrees either), tens of thousands of people mobilized to protest, occupying buildings and schools. In one case, a performance artist burned tuition contracts, essentially freeing the holders of their debts.

The country is smaller than the US and university admissions outcomes are more neatly determined, and it’s possible to systemically link records of college applicants to earnings outcomes. All of this makes Chile an ideal environment to study educational reform, says Chicago Booth’s Seth Zimmerman, who is one of several researchers focusing there: “Institutional features of the way the Chilean higher-education system operates presented an opportunity to learn about how things were operating in both countries in a way you couldn’t do in the US.”

Say you have a student considering college. Which will more greatly affect whether she goes for that degree: her upbringing, or her ability to pay for school?

Pedro Carneiro, now of University College London, and James Heckman, the University of Chicago’s Nobel Prize–winning economist, argued in research from 2003 that what matters most is upbringing. Family factors such as income and background affect whether a student pursues higher education, they say; students from well-off families accumulate skills and knowledge that they use to get into and graduate from college. In this construct, affordability is a secondary factor. “At most 8 percent of American youth are credit constrained in the traditional usage of that term,” they write.

But Chile’s decision to make loans widely accessible offered a way to revisit those conclusions, says Alex Solís, a Chilean economist who teaches at Uppsala University in Sweden. “For me it was kind of obvious to see that people [in Chile] were credit constrained and that’s why they didn’t invest optimally in college education and human capital more generally,” he says.

Traditionally, in Chile, the rich could afford tuition, the poor qualified for subsidized loans, and students in the middle of the income spectrum had little access to grants or affordable loans. Student-loan reforms aimed to change that, offering a social scientist’s favorite experimental setup: a natural treatment group (the students who qualified for the loans) and a control group (those who didn’t). Because cheap government loans went to students who scored above a defined level in the admissions tests, Solís was able to look at data from students who scored just above and just below the cutoff. Students above the cutoff had access to credit, while those below had no ability, functionally, to borrow for college. If students just above the cutoff enrolled in college at a statistically significant higher rate, it would indicate that the availability of credit played into their decision.

The cutoff for the loan program was set at the mean score of students from the poorest fifth of families, and the loans were open to all students except the richest 20 percent. Poor students typically didn’t have access to private loans, which are available in Chile only to elite students who score at the top of the test rankings.

According to Solís’s data, the college-enrollment rate just above the cutoff was double what it was just below the cutoff. After the government increased loan access, enrollment rates were the same in every income quintile, he finds. “Access to loans explains all the college enrollment gradients by family income that exist around this cutoff,” Solís says.

Solís argues that a policy providing more loans to qualified students will allow them to invest optimally in education, increasing their lifetime earnings and affecting their children as well as the GDP. “More human capital implies higher growth rates,” he says.

Moreover, his findings indicate that adding grants to the mix won’t necessarily improve students’ educational attainment. Some students who scored high enough on the admission test qualified for grants in addition to loans. But those grants had no impact on whether or not the students enrolled in college. This suggests that if loans made it possible for students to attend college, those who wanted to attend would do so, regardless of the cost. “That means the main problem here is credit access,” Solís concludes.

Regardless of how students pay for college, however, they want their investment to pay off. It can help to guide students toward degrees and professions that pay more, other research suggests. “It’s not that we don’t want students to be poets; it’s that we think students who choose to be poets should know what the career trajectory for that field typically looks like,” Zimmerman says.

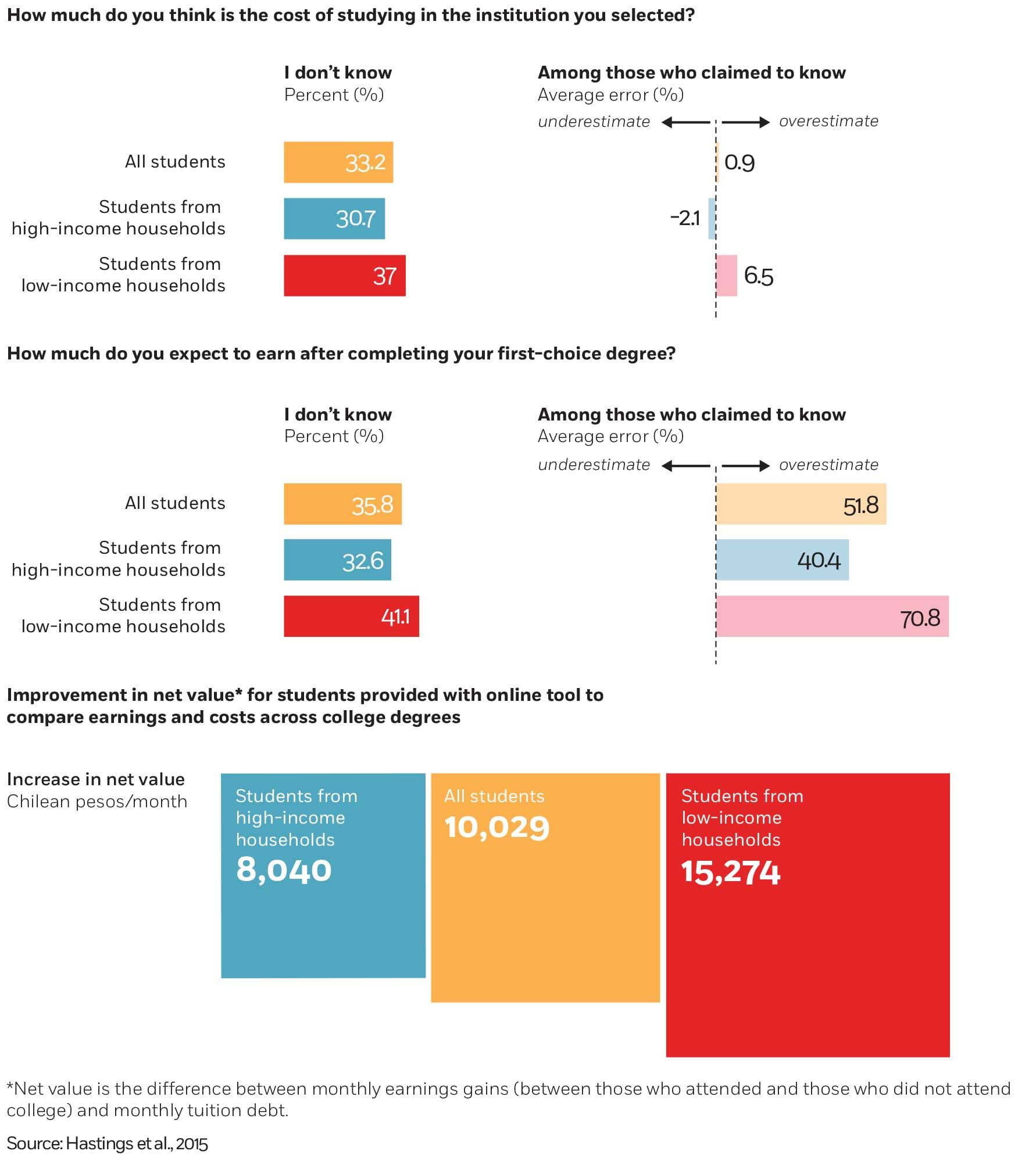

Brown University’s Justine S. Hastings, Princeton’s Christopher Neilson, and Zimmerman worked with Chilean authorities to learn more about how much some degrees are worth in the labor market, and whether that information could sway students’ decisions of what to study. To do this, they needed considerable amounts of data to see who was going to college, how those students performed in high school, where they enrolled in college, how quickly they graduated, and what their income was after graduation. Many of the required records were on paper and had to be digitized. Some of their research was done with the National Education Council’s Anely Ramirez.

The researchers began by looking at 1,100 degree programs, to determine how they affect what graduates earn. The findings support what many parents have counseled their children: you’ll earn more with a medical degree than you will with an art degree, and a degree from an elite school is worth more than a degree from a lesser one. “These results suggest that just failing to be admitted to a program of choice could be one of the luckiest or unluckiest events for a student’s expected future earnings,” the researchers write. They also find that a competitive business degree will produce more of an earnings bump for rich students than poor ones.

It’s one thing to hear this from parents, but would data about costs and earnings outcomes influence college applicants deciding what to study? The researchers gathered survey data from 49,166 federal-student-loan applicants about students’ plans, expected future earnings, and beliefs about tuition costs. Then they offered a randomized group of college applicants an online tool that gave them personalized information about the degree programs they were investigating, including how much past graduates went on to earn and to owe. In case an applicant wanted to see whether she could earn more and owe less in another program, she had access to a database where she could compare results for other programs that admitted students with similar test scores. The researchers then looked at students’ final school choices.

Students knew very little about the earnings and cost outcomes of their degree choices, the findings suggest. Respondents from low-income households were particularly optimistic, overestimating their short-term earning outcomes by more than 70 percent on average. While the effect was limited, giving students access to the information did make a difference, closing about 40 percent of the gap in predicted earnings outcomes between poor and rich students who tested similarly. The extra amount students went on to earn more than justified the cost of implementing the disclosure program.

The goal, of course, is for students who graduate to see the investment pay off and become productive members of society. Disclosure could help, but it’s also important to maintain quality standards at universities, particularly in the midst of major educational reforms.

Influenced by the work of Heckman and the late Gary S. Becker, another Nobel Prize winner, from Chicago Booth, Sergio Urzua of the University of Maryland looked at administrative records to compare poverty rates, income inequality indices, residential decisions, and access to schools. The analysis looked at the net returns of higher education, taking into account the money not earned while in school, the cost of tuition, and the length of degree programs.

He argues that a college education failed to pay off for all Chileans who attended. “Estimates using the most recent information suggest that between 10 percent and 40 percent of the individuals could have been financially better off if they had not attended a higher-education institution in Chile,” he says.

Urzua attributes this to reasons of both demand and supply. On the demand side of the equation, the cohort of new students going to university in Chile now includes a greater percentage from lower socioeconomic backgrounds. This group was likely to have received an elementary and high-school education that was “definitely mediocre,” if not poor, Urzua says. Their ability to face the challenges of college was limited.

On the supply side, an increase in university places has come with detrimental effects on the quality of the education, he says: “You went to college for five years, you got a degree, you got loans to pay for it, and the labor market learned very quickly that your degree did not really have the value you thought it had, and that’s a challenge,” he says. Urzua fingers what he calls “a poorly designed regulatory system.” He cites cases of public universities using false advertising and private universities that ran into financial trouble due to mismanagement.

Chile’s rapid push into mass higher education had consequences. Peru, which is also undertaking a program to increase access to higher education but lags Chile by 15 years, in January 2015 created a national agency tasked with maintaining quality standards in higher education. Chile’s President Michelle Bachelet, reelected in 2013, has proposed but not yet implemented a similar quality-assurance program for Chile.

Around the globe, countries are wrestling with how to fund universities sustainably and produce graduates who will grow their economies. And some of the world’s biggest economies are struggling with the challenge of educating people without saddling graduates with debilitating debt. The BBC has reported about worries of “an army of educated unemployed that some fear could destabilize” the economies of India and China.

In the US, a college degree has become an expectation of the middle class, and student loans persist even through bankruptcy. Economists have warned that unsustainable student-loan debt could cause another financial crisis, much as subprime housing debt did in 2008, with debt potentially hampering individuals’ ability to borrow to buy houses or cars, or otherwise feed the economy. “It’s not possible to have such a large group of the population entering the labor force with such a big debt behind them,” University of Paris economist Thomas Piketty told the news site Big Think.

In 2013, President Barack Obama dedicated part of his State of the Union address to announcing a disclosure program similar to the one test-driven in Chile: a college scorecard that students can use to “compare schools based on a simple criterion—where you can get the most bang for your educational buck,” as he put it. The college scorecard website allows users to learn about many programs’ costs, and some graduates’ incomes.

Chile continues to pioneer educational reforms and generate more data to analyze and learn from. While Vermont Senator Bernie Sanders has advocated for college to be free in the US, President Bachelet has already begun to fulfill a campaign promise to make higher education free, an action that has thrown the country’s universities, most of them private, into turmoil as policy makers scramble to figure out how they will implement the change, and how Chile will pay for it. In March, 200,000 students from Chile’s poorest families began attending university without having to pay fees.

Solís prefers offering more loans to making higher-education free, saying that in Chile, only some students at the lower end of the income spectrum will qualify for a free university degree, meaning there may no longer be financial aid for other groups: “That may create some distortions.”

“Even if college were free . . . you would want students to make informed choices about what to study.”

Eliminating tuition, says Zimmerman, could make disclosure programs even more important than before. “Even if college were free—in fact, perhaps especially if it were free—you would want students to make informed choices about what to study,” he says.

Informed consumers

Though many Chilean students lacked an understanding of the true costs and earnings prospects of their courses of study, giving them the relevant information significantly raised the net value of their educational choices, with students from low-income households benefiting most.

Many Americans think Big Tech should be more tightly regulated, and politicians across the aisle agree. But what exactly should be done?

Break Up Big Tech?

Regular, continuous care is good for patients, and could also benefit providers and insurers.

How Proactive Healthcare Can Save on Costs

Exploring a counterintuitive notion of monetary policy

Will the Fed’s Rate Hikes Raise Expected Inflation?Your Privacy

We want to demonstrate our commitment to your privacy. Please review Chicago Booth's privacy notice, which provides information explaining how and why we collect particular information when you visit our website.