Growth Expectations Drive Stock Prices? It May Be the Other Way Around

Share-price changes may have less to do with fundamentals than conventionally thought.

Growth Expectations Drive Stock Prices? It May Be the Other Way AroundHow private-equity firms lose when they manipulate returns

Private-equity firms trying to raise new capital sometimes overstate fund returns, but investors aren’t fooled.

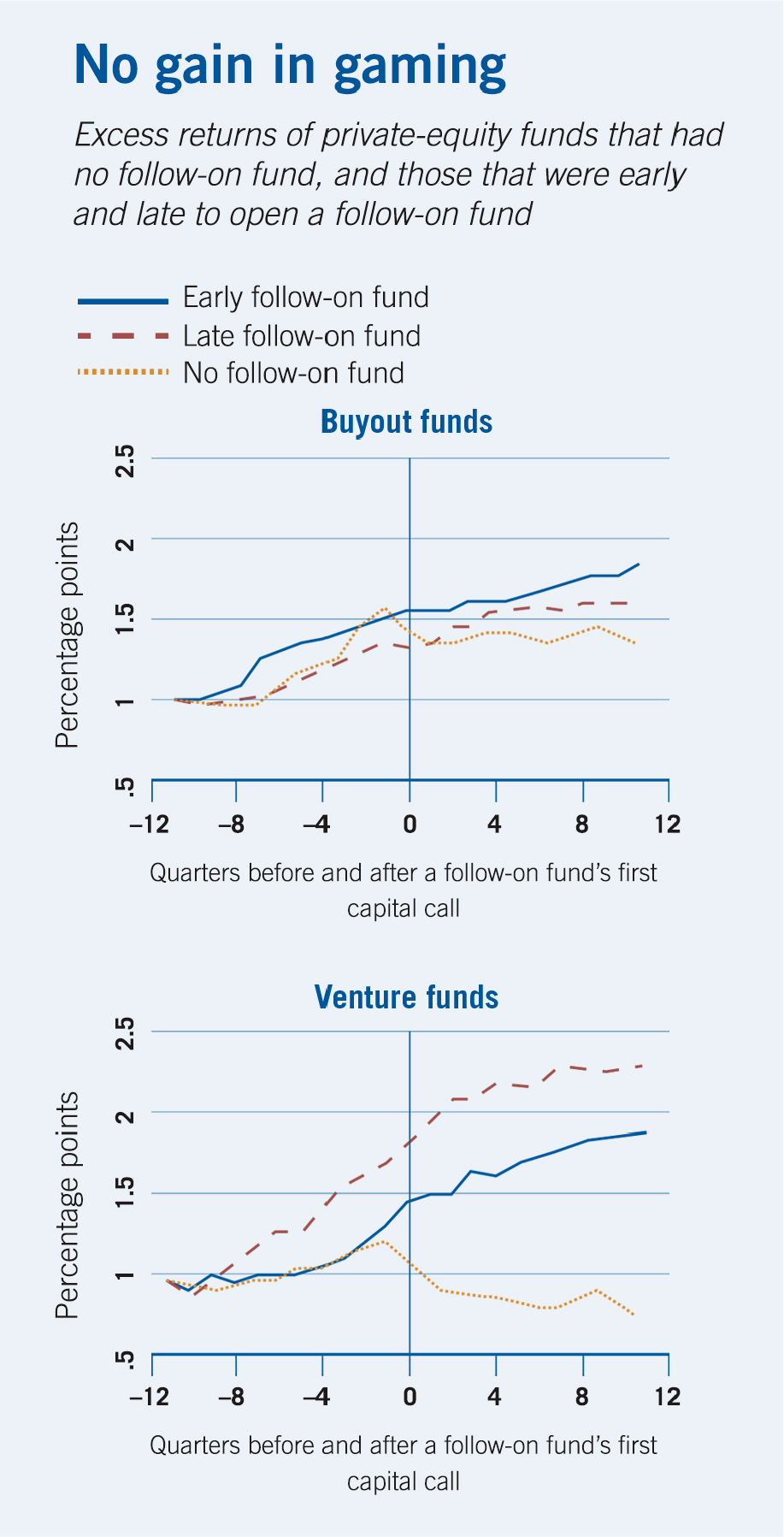

Research suggests that while some underperforming private-equity fund managers overstate asset values, managers at the best-performing funds tend to understate returns.

Gregory W. Brown, Oleg R. Gredil, and Steve Kaplan, “Do Private Equity Funds Game Returns?” The University of Chicago Booth School of Business working paper, October 2013.

Share-price changes may have less to do with fundamentals than conventionally thought.

Growth Expectations Drive Stock Prices? It May Be the Other Way Around

Revisiting a conversation between Eugene F. Fama and Richard H. Thaler on the efficiency of financial markets.

Is the Price Right? Two Nobel Laureates Debate How Markets Work

How can we contend with all we don’t know about the interplay of climate science and economics?

Confronting Uncertainty in Climate PolicyYour Privacy

We want to demonstrate our commitment to your privacy. Please review Chicago Booth's privacy notice, which provides information explaining how and why we collect particular information when you visit our website.