Is There a Ceiling for Gains in Machine-Learned Arbitrage?

An analysis of stock returns tests the limits of A.I.

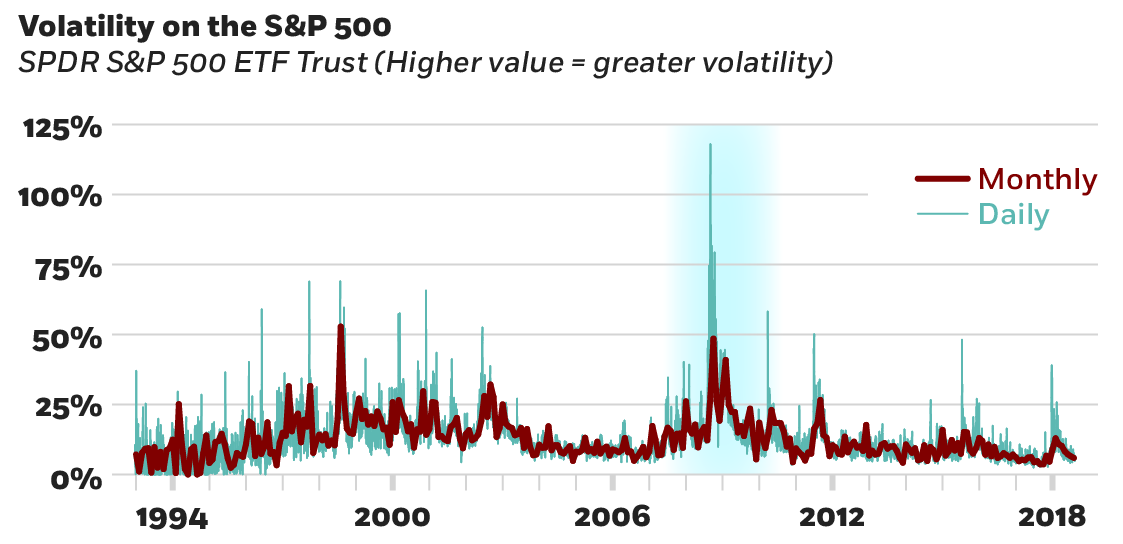

Is There a Ceiling for Gains in Machine-Learned Arbitrage?How to gauge volatility, one asset at a time

An analysis of stock returns tests the limits of A.I.

Is There a Ceiling for Gains in Machine-Learned Arbitrage?

Private debt funds are filling a $1 trillion hole in the lending market for middle-market businesses that can’t get conventional bank financing.

With Business Loans Harder to Get, Private Debt Funds Are Stepping In

They’ve applied millions of ‘disaster flags’ to credit files, masking missing payments.

How Lenders Are Providing Natural-Disaster InsuranceYour Privacy

We want to demonstrate our commitment to your privacy. Please review Chicago Booth's privacy notice, which provides information explaining how and why we collect particular information when you visit our website.